How to Create a Money Lending App: Development Tips and Costs

Updated 06 Mar 2026

13 Min

17478 Views

How to create a money lending app? P2P loan solutions make it possible to lend money anytime for anyone, and that’s why these apps are becoming pretty trendy in the FinTech world. For you as a financial business, a custom lending app is a convenient option to digitalize the lending process and reach borrowers beyond traditional banking channels, as many users prioritize a digital-first experience.

Here’s a concise money lending app development roadmap:

- Step 1. Find a reliable FinTech software vendor

- Step 2. Define your lending app requirements

- Step 3. Make an intuitive lending app design

- Step 4. Go through the lending app development

- Step 5. Launch your lending app

The Cleveroad team has delivered high-quality FinTech software solutions for over 15 years now. In this guide, we’ll help you define how to create a loan app, understand its work principle and potential cost, and help you seamlessly navigate the FinTech regulatory landscape.

What are Lending Apps and How They Work?

P2P (peer-to-peer) lending is a lending model where individuals issue and receive loans directly within the app, without relying on traditional financial institutions such as banks. Most commonly, the process is facilitated by digital mobile loan apps that connect borrowers with potential lenders.

Users can participate either as lenders providing funds or as borrowers requesting loans. While the majority of loans on P2P platforms are funded by private individuals, some platforms also allow companies to participate as lenders or borrowers.

Interest rates can be fixed by the platform or determined through mechanisms such as reverse auctions. In an auction model, borrowers indicate the maximum interest rate they are willing to accept, while lenders compete by offering funding at lower rates.

Let’s review the main use cases for money lending app development:

P2P lending

Connect private investors with borrowers seeking personal loans

Digital micro-lending services

Designed for quick, small loans with simplified approval processes

Consumer credit platforms

Offering installment loans or buy-now-pay-later solutions

SME lending platforms

Help small businesses access alternative financing

Marketplace lending

Here multiple lenders fund a single loan request

DeFi lending

Enable decentralized lending and automated smart-contract settlements

Platform providers that build and operate peer-to-peer lending software earn revenue through service fees. These fees may include fixed charges for borrowers or a small percentage of the loan amount collected from both borrowers and lenders. This platform-based approach explains how modern lending apps monetize digital lending services.

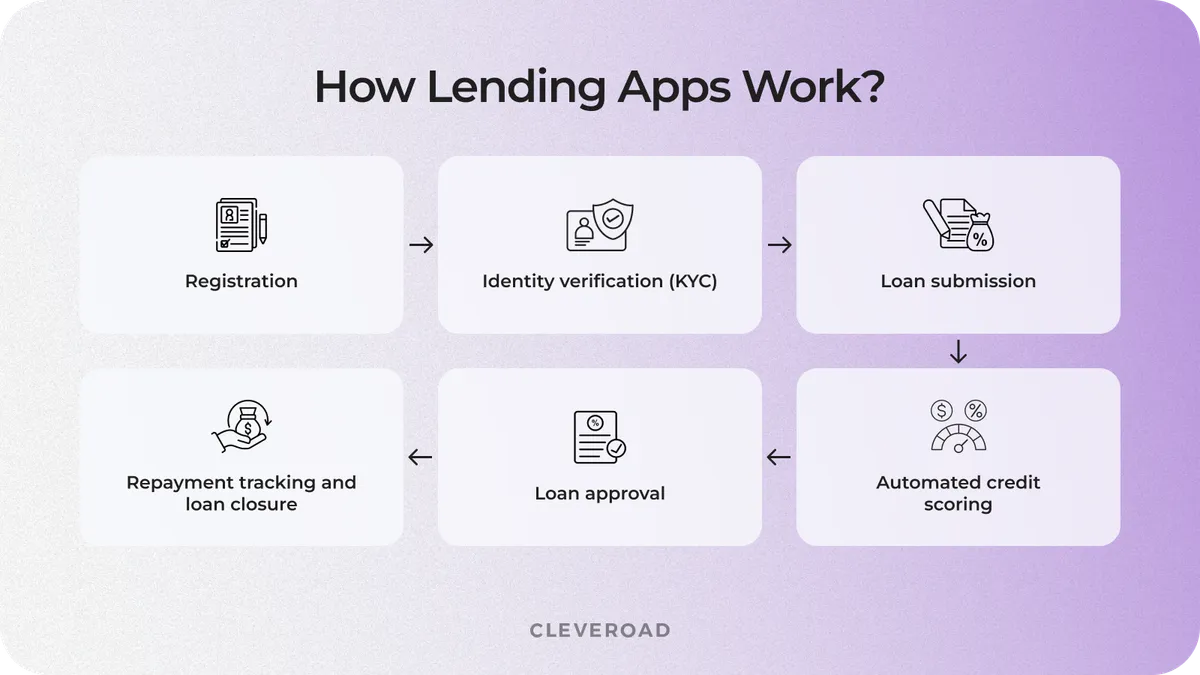

How do money lending apps work?

Money-lending apps automate the entire lending lifecycle, allowing borrowers to request funds and have financial institutions issue loans through a secure digital platform. By integrating identity verification and payment processing tools, these apps simplify the borrowing experience and help financial businesses manage risks and approvals more efficiently. Here’s a brief lending app workflow:

- Registration. Users create an account in the lending app by providing basic personal information and setting secure login credentials.

- Identity verification (KYC). The platform verifies the user’s identity through Know Your Customer procedures. This may include uploading documents and performing biometric verification.

- Loan submission. Borrowers submit a loan request directly through the app by specifying the desired loan amount, repayment term, and purpose.

- Automated credit scoring. The lending platform analyzes the borrower’s financial profile using algorithms and credit data sources.

- Loan approval. If the borrower meets the required criteria, the platform approves the loan and generates digital loan terms.

- Repayment tracking and loan closure. The app monitors repayment schedules, sends reminders, and processes payments through integrated gateways.

How money lending apps work

Types of Money Lending Apps

Money-lending apps come in various forms, catering to diverse user needs and regulatory environments. Choosing the right type depends on your business focus, whether it’s peer-to-peer lending, business financing, short-term microloans, or integrated digital banking solutions. Below are the main types of money lending apps, their definitions, and real-world examples.

| Type of lending app | Distinctive features | Best for |

P2P Lending | Connects borrowers and lenders directly; automated credit checks | Individuals and alternative investors |

Microloan Apps | Small, short-term loans; fast approval | Users needing urgent cash or in emerging markets |

Business Lending | Working capital and credit lines; integrates with accounting systems | SMBs needing capital |

Digital Banking Lending | Full digital banking with loans; seamless account integration | Digital-first users wanting all-in-one banking |

Peer-to-Peer (P2P) lending apps

P2P lending apps connect individual borrowers directly with lenders, bypassing traditional financial institutions. These platforms allow users to request loans and investors to fund them at agreed-upon interest rates.

Real-world example: LendingClub provides an online marketplace where borrowers can apply for personal loans, and investors fund them, earning interest. The platform handles credit checks, payment processing, and regulatory compliance.

Microloan apps

Microloan apps provide small, short-term loans, often targeting underserved populations or urgent financial needs. These loans typically have quick approval processes and are repaid in a short period.

Real-world example: Tala offers instant microloans to users via mobile phones in emerging markets, using alternative data for credit scoring and delivering funds digitally to bank accounts or mobile wallets.

Business lending apps

These apps cater to small and medium-sized businesses (SMBs), offering working capital, invoice financing, or business expansion loans. They often integrate with accounting and ERP systems for seamless financing.

Real-world example: Kabbage (by American Express) provides automated business loans and lines of credit, analyzing business data like bank transactions and invoices to offer instant funding tailored to each SMB’s financial profile.

Digital banking lending apps

Digital banking apps combine traditional banking services with integrated lending features, allowing users to borrow money directly within their banking ecosystem. These apps often include personal loans, credit lines, and overdraft facilities.

Real-world example: Chime, a digital neobank, offers its users early access to earned wages and credit-building loans, all within a fully digital banking experience that integrates payments, accounts, and lending.

We provide custom FinTech software development services. Check out our service page to learn how, together, we can create an intuitive and secure lending app experience

How to Create a Money Lending App?

Creating a money lending app requires careful planning and adherence to financial regulations. When done well, your app can attract both borrowers and lenders, and help your FinTech business scale efficiently.

Step 1. Find a reliable FinTech software vendor

Choosing the right vendor is critical for your success. You need a partner who understands lending workflows and secure payment integrations to translate your business goals into a reliable technical solution.

When evaluating a vendor, pay attention to several key criteria:

- FinTech experience: proven expertise in lending or financial platforms

- Legal knowledge: familiarity withessential regulatory and data protection requirements

- Technical expertise: ability to build secure and scalable architectures

- Transparent processes: clear cost estimation and development methodology

- Flexible cooperation models: options like dedicated teams or staff augmentation

Additionally, review the vendor’s communication practices and ability to provide business analysis and solution architecture. For example, at Cleveroad we have 15+ years of experience helping businesses deliver modern and secure FinTech software solutions.

One example is our collaboration with Mangopay, an Irish-based company that delivers payment infrastructure for more than 2,500 European platforms, including Vinted and Rakuten. With the help of Advent International, the company provides flexible payment solutions tailored for C2C, B2C, B2B, and marketplace ecosystems.

Within the IT staff augmentation model, our specialists assisted Mangopay in upgrading its payment platform and introducing a new FinTech product aligned with strict security and regulatory requirements, including KYC and AML standards. As a result, we helped deliver a unified solution for global money transfers that includes multi-currency pricing, digital wallets supporting multiple currencies, treasury management tools, and international payout capabilities.

Here’s what Kirk Donohoe, CPO at Mangopay, says about collaboration with Cleveroad team:

Kirk Donohoe, CPO at Mangopay, provides feedback about collaboration with Cleveroad

Step 2. Define your lending app requirements

After selecting a reliable vendor, the next step is to define your lending app requirements together. The vendor helps you clarify your target audience, loan types, repayment models, and interest calculation methods. Through collaborative solution workshops, you can outline essential features. At Cleveroad, our solution workshop is free, providing guidance on lending models and technical approaches.

Next comes the discovery phase, where business analysts and solution architects refine and document all requirements. This includes user flows, system architecture, feature prioritization, and cost and timeline estimation. As a result, you receive a clear roadmap that guides money lending app development, ensuring the app delivers value to users while staying compliant.

Step 3. Make an intuitive lending app design

Design matters for adoption. You want an interface that is clean, intuitive, and easy to navigate. Borrowers and lenders should be able to view dashboards, submit loan requests, monitor their applications, and manage payments without confusion. We at Cleveroad ensure that your app design follows FinTech best practices, optimizing usability while maintaining security and accessibility across devices.

Step 4. Go through the lending app development

During development, focus on building a secure and scalable architecture for your chosen platforms, whether iOS, Android, or web. Cleveroad works closely with you to implement core functionalities while ensuring the app handles sensitive data safely. Our team manages development, testing, and deployment processes, keeping your platform robust and compliant with regulations.

We also prioritize user experience and system reliability. We thoughtfully integrate features like credit scoring and payment processing so your app runs smoothly without overwhelming users.

Step 5. Launch your lending app

Once the app is ready, it’s time to deploy. You monitor how users interact with it, gather feedback, and make iterative improvements. At Cleveroad, we continue to support you after launch, providing maintenance and guidance on updates and evolving financial rules. This ensures your platform grows securely and remains a reliable tool for your business and app users alike.

What Legal Requirements are a Must During Lending App Development?

When developing a money lending app, you must comply with various legal frameworks to ensure data security, user privacy, and regulatory approval. Compliance not only protects your users but also builds trust and minimizes the risk of fines or operational restrictions.

GDPR compliance

The General Data Protection Regulation (GDPR) governs how personal data of EU residents is collected, stored, and processed. You need to implement clear consent management, allow users to access or delete their data, and ensure secure storage and transfer. Adhering to GDPR compliance reduces legal risks and reassures users that their sensitive financial information is handled responsibly in your money lending app development.

ePrivacy

The ePrivacy Regulation complements GDPR by regulating electronic communications and cookies. You must ensure secure messaging, obtain proper user consent for tracking technologies, and protect digital communications. Compliance helps maintain privacy and transparency in all digital interactions within your lending app.

CCPA

The California Consumer Privacy Act (CCPA) gives California residents control over their personal data. You must provide mechanisms for users to view, delete, or opt out of data collection and sales. Compliance enhances transparency, strengthens user trust, and ensures that your app can operate freely in the California market.

KYC, FINMA, FMIA

Know Your Customer (KYC) procedures and financial regulations, such as FINMA (Switzerland) and the FMIA (Swiss Financial Market Infrastructure Act), are crucial for preventing fraud, money laundering, and financial misconduct. You need robust identity verification, transaction monitoring, and secure data handling to meet these standards. Implementing these safeguards ensures regulatory approval to operate across multiple international jurisdictions.

At Cleveroad, we thoroughly create solutions that meet all essential FinTech domain regulations.

For example, we helped a Swiss bank modernize its online banking system for investment and trading services, supporting both B2B and B2C clients. Our team built a custom ecosystem with easy sign-up and a web portal for trading and investing.

We designed the solution with a refined architecture that integrates all client workflows while ensuring full compliance with FINMA and FMIA regulations. By implementing KYC procedures and need-to-know access control, the bank can now scale efficiently, operate securely under its existing license, and provide a seamless, compliant experience for its users.

Feel free to learn more details about the eBanking software system development for a Swiss bank in our case study

DORA

The Digital Operational Resilience Act (DORA) sets standards for ICT risk management in financial services. Lending apps must have cybersecurity measures, business continuity plans, and incident reporting processes. DORA compliance during assessing how to make a loan application ensures operational resilience and protects your platform from cyber threats and systemic failures.

ISO/IEC 27001:2013

ISO/IEC 27001:2013 provides an international framework for information security management. You should establish policies, access controls, encryption, and audit processes to protect sensitive financial and user data. Aligning with ISO/IEC 27001:2013 demonstrates your commitment to data security and risk management.

Cleveroad is an ISO/IEC 27001:2013–certified development partner, ensuring that our software solutions meet essential global security standards. You can read our article to learn more.

How Much Does it Cost to Create a Loan Lending App?

Money lending app development costs depend on many factors, including design complexity, QA services, and the cooperation model you choose. The location of developers also plays a major role in pricing. For example, in Central and Eastern Europe, where most of Cleveroad’s developers are located, the average hourly rate is around $50. A money-lending app creation price here can start at approximately $25,000 and reach up to $100,000+, depending on features and functionality.

You can review our lending app time-and-cost estimation table for a more precise overview.

| Lending app complexity | Lending app development time (h) | Estimated cost ($) | Features included |

Basic lending app | 500-700 hours | $25,000-$35,000 | Core lending functionality, user registration, loan submission, basic credit scoring, repayment tracking |

Medium lending app | 800-1,200 hours | $40,000-$60,000 | All Basic features + automated credit scoring, KYC verification, notifications, payment gateway integration |

Advanced lending app | 1,400-2,000 hours | $70,000-$100,000+ | All Medium features + AI-powered risk analysis, personalized lending offers, advanced analytics dashboard, multi-platform support (iOS, Android, web) |

To get a clear and accurate estimate of your money lending app development cost and overall budget, you can schedule a consultation with our Senior Business Development Manager from the FinTech Unit. During this session, we’ll review your project requirements, suggest the best technical approach, and provide a detailed cost breakdown tailored to your app’s complexity and desired features.

How Cleveroad Can Help You With Lending App Development?

Cleveroad is a FinTech software development company based in the CEE region, specializing in building secure and compliant money lending and P2P loan solutions. Our team brings extensive experience in creating apps that meet regulatory standards while delivering smooth user experiences.

Here are the main benefits you’ll get when you partner with us for your lending app development:

- Partnership with an ISO-certified team, including ISO 27001:2013 for robust information security and ISO 9001:2015 for mature quality management.

- Proven expertise in FinTech and lending app development, ensuring compliance with regulations such as KYC, FINMA, FMIA, GDPR, and CCPA.

- Flexible cooperation models tailored to FinTech, including dedicated development teams and IT staff augmentation.

- Integration with third-party financial services and APIs for payments, credit scoring, and automated loan management.

- Access to end-to-end FinTech app services, from building apps from scratch to software modernization, cloud deployment, UI/UX design, and IT consulting.

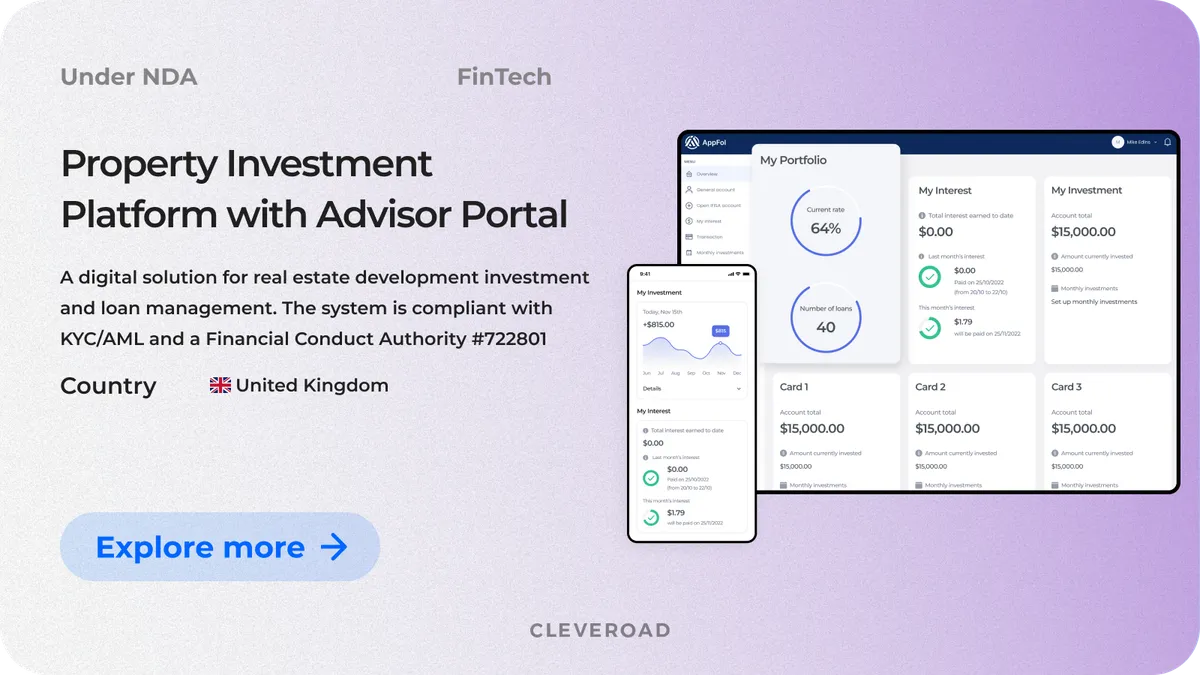

To demonstrate our capabilities in the lending and FinTech space, we’d like to highlight a recent project we worked on: a platform for managing property investments.

A platform for managing property investments designed by Cleveroad

Our client is a UK-based conglomerate with over 22 years of experience in property investment. They needed a digital solution to manage funds, investors, and real estate projects more efficiently, as their in-house resources were insufficient for building a comprehensive platform covering all investment workflows.

To address the client’s business goals, Cleveroad supported the project by:

- Developing a full ecosystem including mobile apps (iOS and Android), a web-based Advisor portal, and an Admin backoffice to cover all investment flow processes.

- Ensuring regulatory compliance with KYC/AML standards and the Financial Conduct Authority #722801, including identity verification, account validation, and transaction monitoring.

- Designing custom UI/UX for seamless navigation and modern, user-friendly interfaces for investors, advisors, and property developers.

- Enriching the customer’s team through the Dedicated Team model, providing solution architects, developers, QA engineers, and DevOps specialists to ensure timely and high-quality delivery.

- Implementing robust backend architecture to support secure transactions, account management, and investment tracking across multiple stakeholders.

Results for the client: Our customer received a fully functional, industry-compliant investment platform. It covers all stakeholders, including individual and institutional investors and property developers. The ecosystem allowed investors to make informed decisions efficiently.

By automating processes and providing secure, scalable infrastructure, the platform reduced operational costs, enhanced investor engagement, and increased fundraising activity. In the first operational year, users invested £164.4M, earning £7.6M, with £9.3M earned in the second year, demonstrating significant growth and ROI.

Build a tailored lending app with Cleveroad experts

Contact us now. Our experience FinTeach software team will help you create a highly secure and user-friendly lending app that matches your tech expectations and budget

To build a well-designed money lending application or personal loan app, follow these steps:

- Find a reliable FinTech software vendor. Choose an experienced partner for fintech app development to build a secure loan lending mobile app and ensure your digital lending platform is scalable and compliant.

- Define app requirements. Decide on loan products and whether your app is a p2p lending platform and supports traditional lending. Clear requirements streamline the application development process.

- Design an intuitive interface. Your loan mobile app should include dashboards for app users. The solution should include features for instant loan requests, applying for a loan, and efficiently obtaining a loan for a smooth lending experience.

- Develop your lending solution. During loan lending app development, integrate KYC and loan repayment tracking. Ensure your loan mobile apps work reliably and support scalable growth in the digital lending market.

- Launch the app. Deploy your mobile lending app and monitor usage. Ensure users can apply for a loan and complete loan repayment, delivering a secure lending solution.

Costs for loan app development vary with design, QA, and development process complexity. Scalable loan apps with AI tools or cross-platform support cost more. At Cleveroad, mobile lending development averages $50/hour, and a loan lending mobile app can start at $25,000-$100,000+, depending on the app complexity.

The timeline for loan lending app development depends on features, platforms, and compliance. A personal loan app can take 3-4 months, while a digital lending platform with advanced credit scoring, AI, and loan repayment tracking may take 6-8 months. Working with Cleveroad ensures application development is timely, secure, and regulatory-compliant.

Loan mobile apps connect borrowers and lenders, automating the lending solution from application to repayment:

- Registration. App users create accounts with secure credentials.

- Identity verification (KYC). Supports the safe obtaining of a loan.

- Loan submission. Borrowers request loans via a loan lending mobile app, selecting the amount, purpose, and repayment.

- Automated credit scoring. Supports decisions for personal loan app loan products.

- Loan approval. Users receive digital terms for instant loans or traditional loans.

- Repayment tracking. The mobile lending app monitors loan repayment and ensures loan mobile apps work smoothly.

Evgeniy Altynpara is a CTO and member of the Forbes Councils’ community of tech professionals. He is an expert in software development and technological entrepreneurship and has 10+years of experience in digital transformation consulting in Healthcare, FinTech, Supply Chain and Logistics

Give us your impressions about this article

Give us your impressions about this article

Comments

4 commentsI want to create a lending app

I want to start Bitcoin loan app

I want to start a lending company and i need a good App and advice to create it

I want to start a micro lending company and I needed to have an app for my clients, I need help building this app, kindly advice Thank you.